Into the default darkness

Into the Default Darkness

By Megan McKee

April 13, 2017

About a month ago, a Louisiana military veteran contacted the country’s consumer protection agency to complain about his treatment by Pioneer Credit Recovery. The company, he said, was “unprofessional and abusive” while attempting to collect on his student loan debt. A representative from the debt collection company owned by student loan giant Navient had called him a liar because the company couldn’t find financial records he had already sent twice. He sent them a third time, despite the collection representative's vulgar language and more accusations of lying. That didn’t stop him from doing the right thing. “I made monthly arrangements and did not miss a payment,” he wrote in his online complaint. And then, another surprise, courtesy of Pioneer. The debt collectors started garnishing his wages. He called the company and “was told the only way to cease garnishment was to make payments on top of monthly wage garnishments.”

The Louisiana veteran is just one of thousands of student loan borrowers who have lodged complaints against Pioneer through the federal Consumer Financial Protection Bureau, or CFPB, which protects consumers and borrowers from predatory, unfair, or illegal practices in a variety of industries. In fact, Pioneer’s behavior rose to a level the bureau deemed so egregious that the CFPB filed suit against Navient and Pioneer in January to address a multitude of allegations they claim has affected tens of thousands.

The veteran had been paying his loans on time, yet was still targeted for wage garnishing. So what happens to borrowers facing dire life circumstances like cancer or job loss while carrying student debt? Or people who have low-paying jobs? After nine months of unsent payments, federal student loans go into default, forcing borrowers into a subset of the loan industry dominated by lucrative federal government contracts worth billions and awarded to private debt collectors, according to federal Department of Education records.

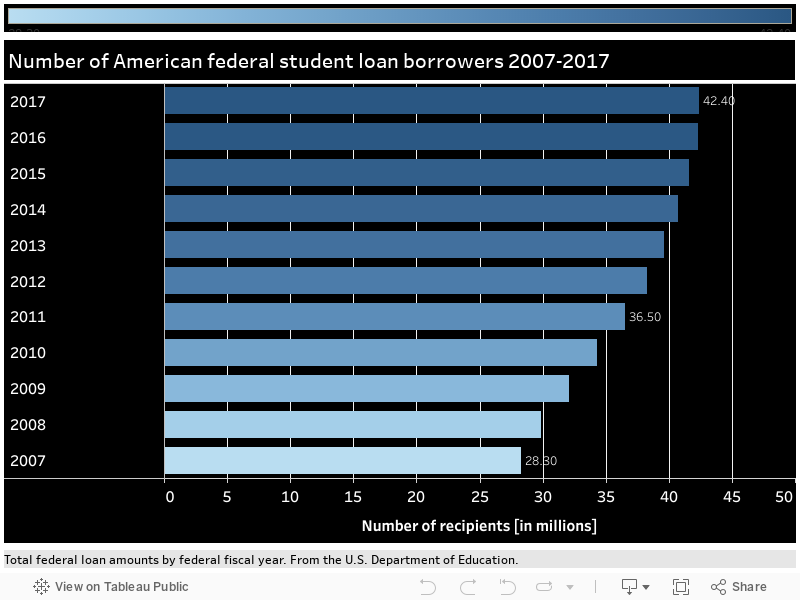

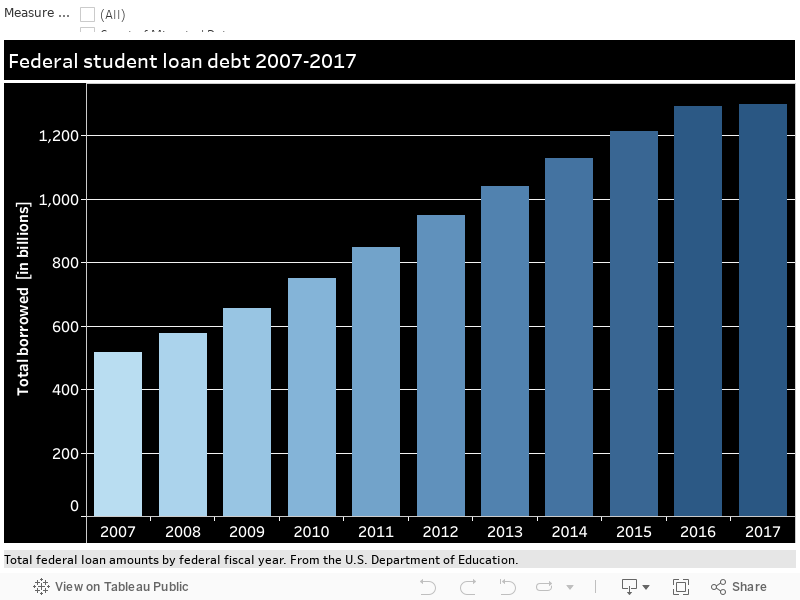

There are about 42.4 million Americans with federal student loan debt totaling $1.3 trillion. The Department of Education’s most recent data reports that the default rate is around 11.3 percent, down from a high of 14 percent during the Great Recession. Using these numbers, we can estimate that 4.8 million Americans have loans in default.

The veteran from the South had been paying his loans on time, yet was still targeted for wage garnishing. So what happens to borrowers facing dire life circumstances like cancer or job loss while carrying student debt? Or people who have low-paying jobs? After nine months of unsent payments, federal student loans go into default, forcing borrowers into a subset of the loan industry dominated by lucrative federal government contracts worth billions and awarded to private debt collectors, according to Department of Education records.

These debt collectors benefit from contract renewals and account portfolios that are entirely dependent on the productivity of its representatives, hourly-paid workers who are tasked with securing money from borrowers who, by the very fact they’ve been referred to a company like Pioneer, are least able to pay.

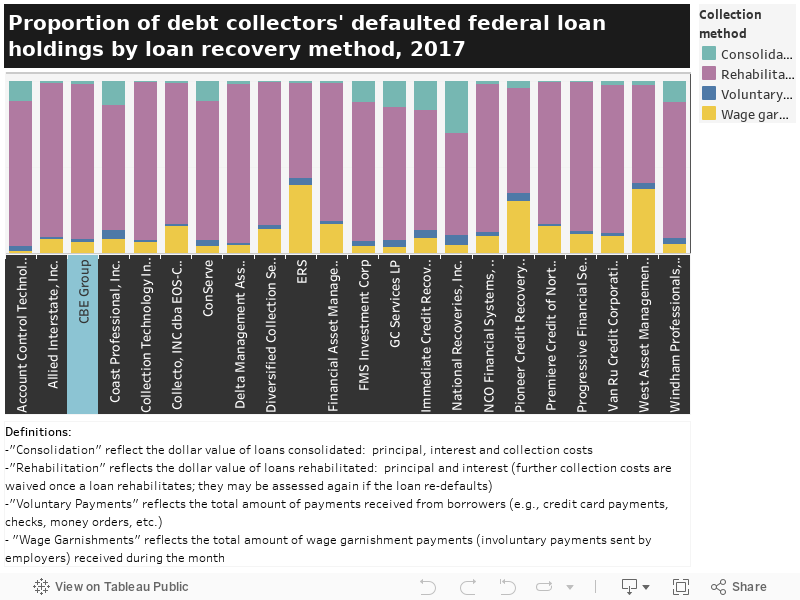

It’s this dynamic that consumer advocates claim inspires rampant illegal loan recovery tactics as collection agencies attempt to collect on their default loan portfolios worth a reported $81 billion. That’s more than half the country’s $131 billion worth of default loans.

The $81 billion is spread, unevenly, among 30 companies. This arrangement is comfortable and lucrative for debt collection companies, but their continued contracts are based on how much money they can glean from the country’s worst-off federal student loan recipients.

If a debt collector leads this government-contracted pack by attaining the highest repayment, the company is entitled to government-funded bonuses and additional defaulted loans to add to their accounts, according to the contracts. This leads to the illegal withholding of information to prioritize money collected over sustainable repayment options, thereby securing their reputations as productive, effective debt collectors. And if a borrower is savvy or lucky enough to enroll in an income-based repayment plans, debt collectors can hide or obscure enrollment deadlines so tose borrowers become ineligible for the very plans that were designed for people like them.

“Given their role in creating the crash, it is reasonable to expect lenders to do everything possible to help borrowers with unaffordable loans,” wrote Deanne Loonin of the National Consumer Law Center in a 2014 report on the history of Sallie Mae and the outrageous actions taken by the company under the guise of helping non-rich students get an education. “We have found private lenders, including Sallie Mae, to be inflexible in granting long-term repayment relief for borrowers. Lenders that had no problem saying “yes” to risky loans are having no problem saying “no” when these borrowers need help.

A deeper look into the companies show curious, if not troubling data like wildly varying rates of wage garnishment, a tactic that allows debt collectors to coordinate with employers to ensure employee borrowers don’t have any say on how much they pay. The other methods for collection tracked by education department data are loan rehabilitation, consolidation, and voluntary payments made by borrowers.

In January, the CFPB filed suit against Navient, formerly known as Sallie Mae, the government’s long-time loan servicer and a for-profit company that’s been the target of scrutiny from multiple government agencies and legal entities for years. In its lawsuit, the bureau alleges that Navient “failed borrowers at every stage of repayment” via shortcuts and deceptions.

Navient denied any wrongdoing in a statement, labeling the allegations “unfounded.”

“The timing of this lawsuit … on the eve of a new administration reflects [the bureau’s] political motivations.” The CPFB alleges that Navient violated several consumer-protection laws by “systematically” steering struggling borrowers into costly forbearances – an option designed for short-term financial crises, not longer circumstances like unemployment or underemployment – rather than the income-based repayment plans designed for consumers who can’t afford traditional payments plans.

For those who managed to get into the borrower-friendly income-based plans, Navient engineered ways that consumers would become ineligible for the plan, according to the CFPB. The bureau’s lawsuit alleges the company “failed to disclose the annual deadline to renew those plans, misrepresented the consequences of non-renewal, and obscured its renewal notice to borrowers who were due for renewal.”

Navient said in its January statement that the company’s federal student loan clients “are 31 percent less likely to default than their peers at other servicers” and that the company is “a leader in advancing policy recommendations to streamline enrollment and reenrollment in income-driven plans.” The company vowed to “vigorously defend against these false allegations.”

Whether or not Navient purposely withheld info, hundreds of thousands of borrowers were immediately harmed by increased monthly payments and if they couldn’t keep up, their credit scores bore the fallout, according to the lawsuit. Tens of thousands of complaints against the company were logged by the consumer bureau, Navient, and other government entities, according to the lawsuit.

There’s more. The CFPB alleges that Pioneer Credit Recovery, Inc., a subsidiary wholly owned by Navient that has overseen $1.9 billion worth of defaulted student loans in the past year and a half, hijacked the student loan system to enrich the company.

Among the other 29 debt collection companies, similar horror stories abound. The CFPB maintains a public consumer complaint database on its website. Since Dec. 2011, more than 31,000 borrowers have submitted complaints about student loan debt collectors.

If indeed the ample testimony of thousands of borrowers is true, one clue to explain the motivation behind abuse of the system can be found in the 78-page federal government contracts: commission.

The government pays debt collection companies a percentage of each payment collected.

Just as commission is a real incentive for people to do their jobs well – for the government, this is measured by the ability of collection associates to get borrowers into a repayment option affordable and sustainable – the company’s earnings are directly tied to the types of loan repayments, according to the government contracts. Debt collectors earn 17.5 percent commission on all non-Direct federal loan payments; 14 percent of money received via wage garnishing; between 12.5 percent and 15 percent for payments on rehabilitated loans; and 6.5 percent on payments toward consolidated loans.

Furthermore, the Department of Education measures each company’s performance based on total money collected and number of accounts served, according to the contracts. The rating system is known under its somewhat Orwellian name: Competitive Performance and Continuous Surveillance, or CPCS.

“The top performers under the [CPCS] set the standards by which all … contractors are measured,” read the contracts. “These high standards drive better performance by all contractors."

In short, it’s a race to the top that forces every contractor to match the top performing companies, no matter which tactics are employed to get those payments.

While the contracts clearly state that commission given on payments illegally obtained will be rescinded by the government, the CPFB’s extensive online database of consumer complaints make clear that the reality of default loan collection doesn’t gibe with the laws that are supposed to help borrowers.

Megan McKee is a writer and grad student in Boston, and she's pretty darn cool.